London November 24 2024: The junk-bond rally in emerging markets risks being just an interlude between the debt crisis of the past four years and a new bout of distress in the next four, if Donald Trump does what he says he will.

A Bloomberg index of high-yielding sovereign dollar debt is heading for a 15% surge this year, the biggest annual gain since 2016. Global investors are rewarding countries such as Argentina, Sri Lanka and Ghana for healing their defaults and embarking on economic reforms. This rally has shown resilience even to the US yield spikes of the past two months.

President-elect Trump’s return to White House has raised doubts about the longevity of that rally. The world’s poorest nations — which form the bulk of the EM junk-bond universe — stand to lose the most from his pledges to raise trade tariffs, boost government spending and deport foreigners without visas. Their dependence on dollar flows means US policy will hit them more than countries that have domestic sources of capital and demand.

“Trump’s anticipated policy changes will likely push the Federal Reserve to pause rate cuts, keeping the global economy in a higher-for-longer interest-rate environment,” said Reza Baqir, a former governor of Pakistan’s central bank and now the Dubai-based head of sovereign-advisory services at Alvarez & Marsal.

“This shift weakens emerging-market currencies against the dollar, amplifying challenges for countries already grappling with economic vulnerabilities. As reserves are depleted and external stability is compromised, these dynamics heighten the risk of financial distress.”

Ratings companies are also watching Trump’s policies for their potential impact on sovereign creditworthiness. Moody’s Ratings, for instance, is paying attention to how much of a “natural flow of dollars” a country has in order to insure against trade disruptions.

“Disruptions to global trade from tariffs and other measures will obviously be bad for emerging markets that export to the US, even if they price their exports in dollar terms,” said Vittoria Zoli, an analyst at Moody’s. “That could be compounded by a strong US exchange rate, particularly if US policy rates stay higher than previously expected.”

Lone Outperformer

Gains in high-yielding bonds have been the brightest spot in emerging markets this year as virtually every other asset in the universe has underperformed. Emerging-market stocks are trading near the lowest level since 1987 relative to US equities. The currency carry trade is losing money and investment-grade bonds continue to be shunned by global investors.

The rally has helped junk bonds cut their average yield by 166 basis points this year to 8.45%, still an attractive additional return over the risk-free rate. At least 31 of the 71 countries in the Bloomberg EM High Yield Total Return Index have had double-digit returns, with four — Argentina, Ecuador, Moldova and Ukraine — generating more than 50%.

The momentum has continued even after US election results, despite Trump’s “America First” pledges. Money managers say they aren’t yet selling the bonds because it’s too early to price in the risks, given the inauguration is still eight weeks away and as Trump may not turn all his campaign rhetoric into action.

“Roughly 50% of what Donald Trump proposed during the election campaign will be implemented,” Luca Paolini, chief strategist at Pictet Asset Management, wrote in a note. So far, the market has only priced in deregulation and tax cuts, he said. “Two big tail risks are underpriced: an all-out global trade war and a surge in bond yields.”

Investors also say emerging-market turnaround stories have more room to go. For instance, bullish bets on President Javier Milei’s fiscal reforms in Argentina or the prospect of an end to the Russian-Ukraine war could continue to generate returns before the realities of a second Trump term materialize.

Some even see pockets of benefits for emerging markets from Trump’s policies, in the form of a faster-growing US economy and diversion of trade from China to smaller nations.

“We will see volatility increase,” said Martin Bercetche, a hedge-fund manager at UK-based Frontier Road. “This should create a good trading environment. Until we get further clarity on the magnitude of Trump’s policies, it’s difficult to have a strong opinion as to where levels will be in the next few years.”

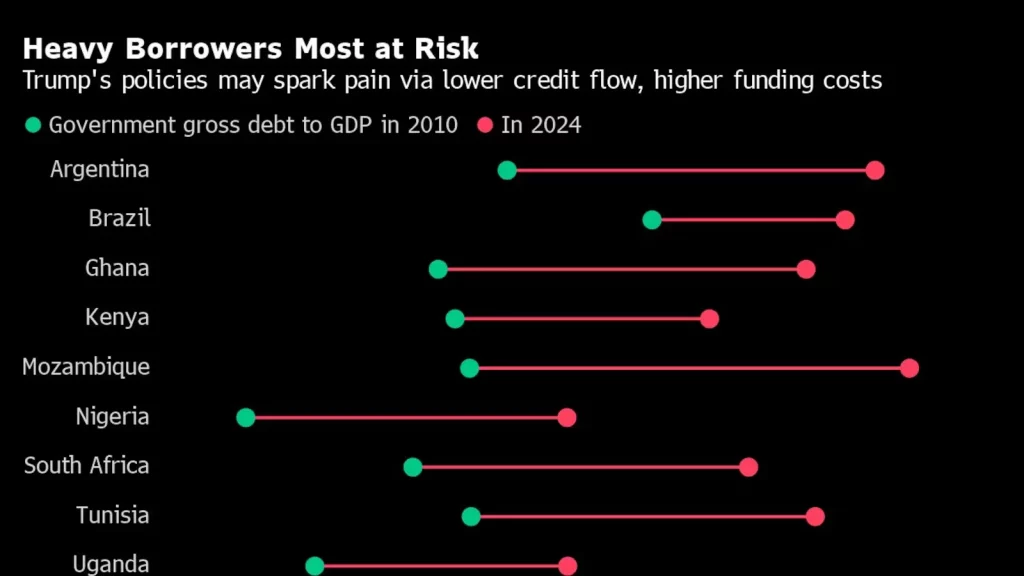

While bond investors are debating near-term fluctuations over Trump’s policy, the key challenge to emerging economies lies in their long-term impact on credit flow. After four years of elevated interest rates and constrained market access, poorer nations can ill-afford any further flight of capital — which is what Alvarez & Marsal expects if Trump’s policies are fully implemented.

The debt adviser’s research shows those countries with high debt levels, high gross financing needs, hidden off-balance-sheet liabilities, an inefficient public sector and facing geopolitical risks are the most vulnerable to a loss of funding. Argentina, Brazil, Ghana and Kenya figure among nations that have seen the sharpest increases in debt burdens over the past decade or more.

Extra Yield

Investors may find the compensation offered by high-yield debt inadequate amid Trump’s policy risks. The securities offer an extra yield over Treasuries of about 585 basis points, close to the levels that sparked a selloff in 2021. They are also the least attractive in six years compared with emerging-market investment-grade bonds.

Trump’s inauguration will bring a fresh assessment of emerging-market creditworthiness. If he shows a zeal to follow through on his pledges, the risk of a new cycle of distress and default will be priced in, calling curtains on the rally that marked 2024.

{kind=link}